Where Did Everyone Go?

Where Did Everyone Go?

The largest post pandemic mystery to me

Let me preface this post to say this was frustrating to write. As soon as I thought I’d found an answer, it would lead to an effective dead end. I’d go down one road to then find myself back where I started.

Maybe that’s how everyone feels right now, there’s not a clear answer to what is going on, but man, it sure feels like everyone disappeared.

I saw yet another article in the WSJ1 about labor shortages throughout the country. I’m sure everyone has had the same experience over the past 18 months, at virtually any services business (restaurant, hotel, retail store) everyone is chronically under staffed. For a while it made intuitive sense, especially during the dog days of the pandemic. A mixture of illness, stimulus checks, and wide-spread financial obligation abatements resulted in a tight labor market.

But what in the world is going on now?

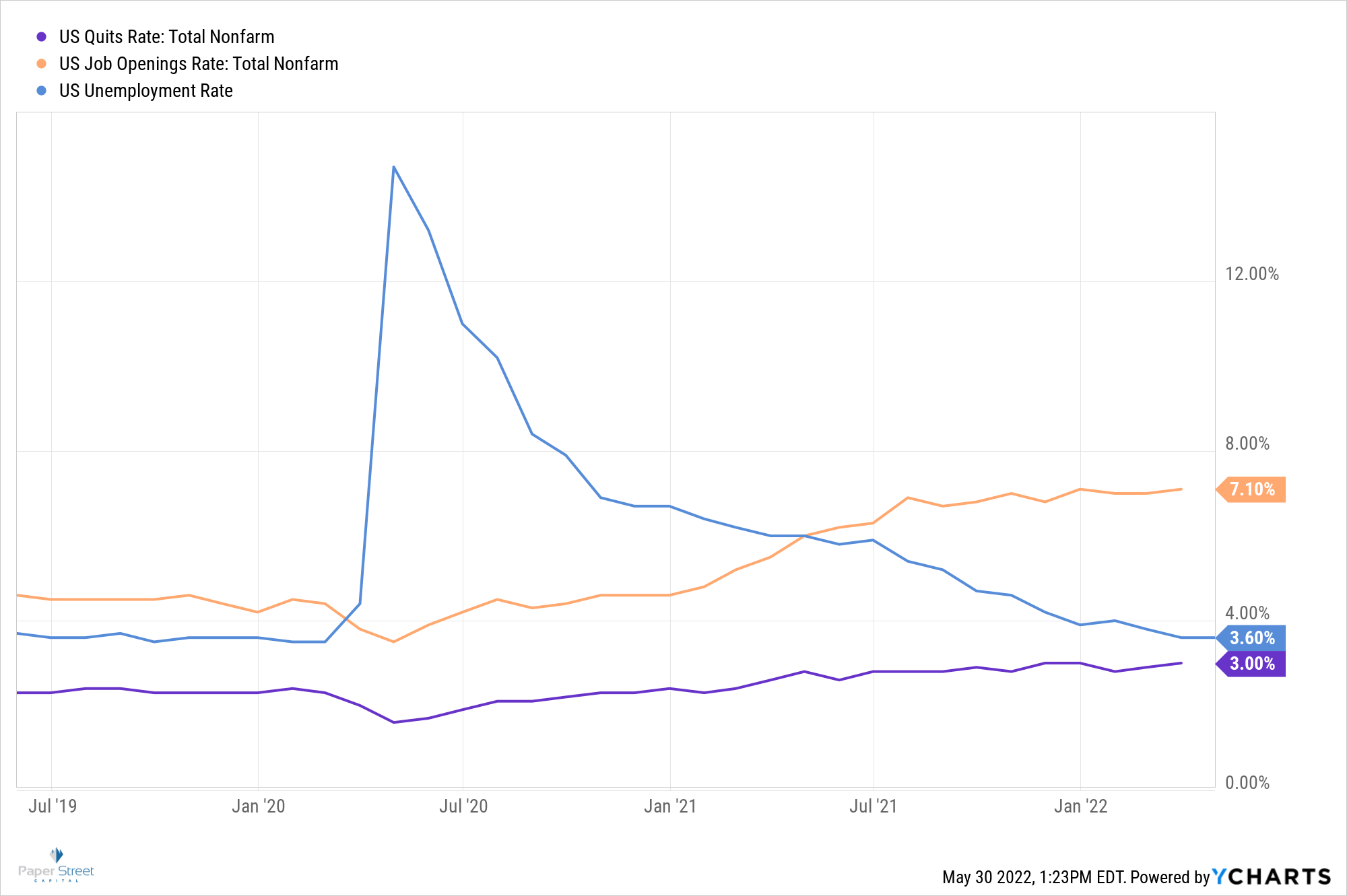

We have an elevated quit rate, coupled with historically high job availability and low unemployment:

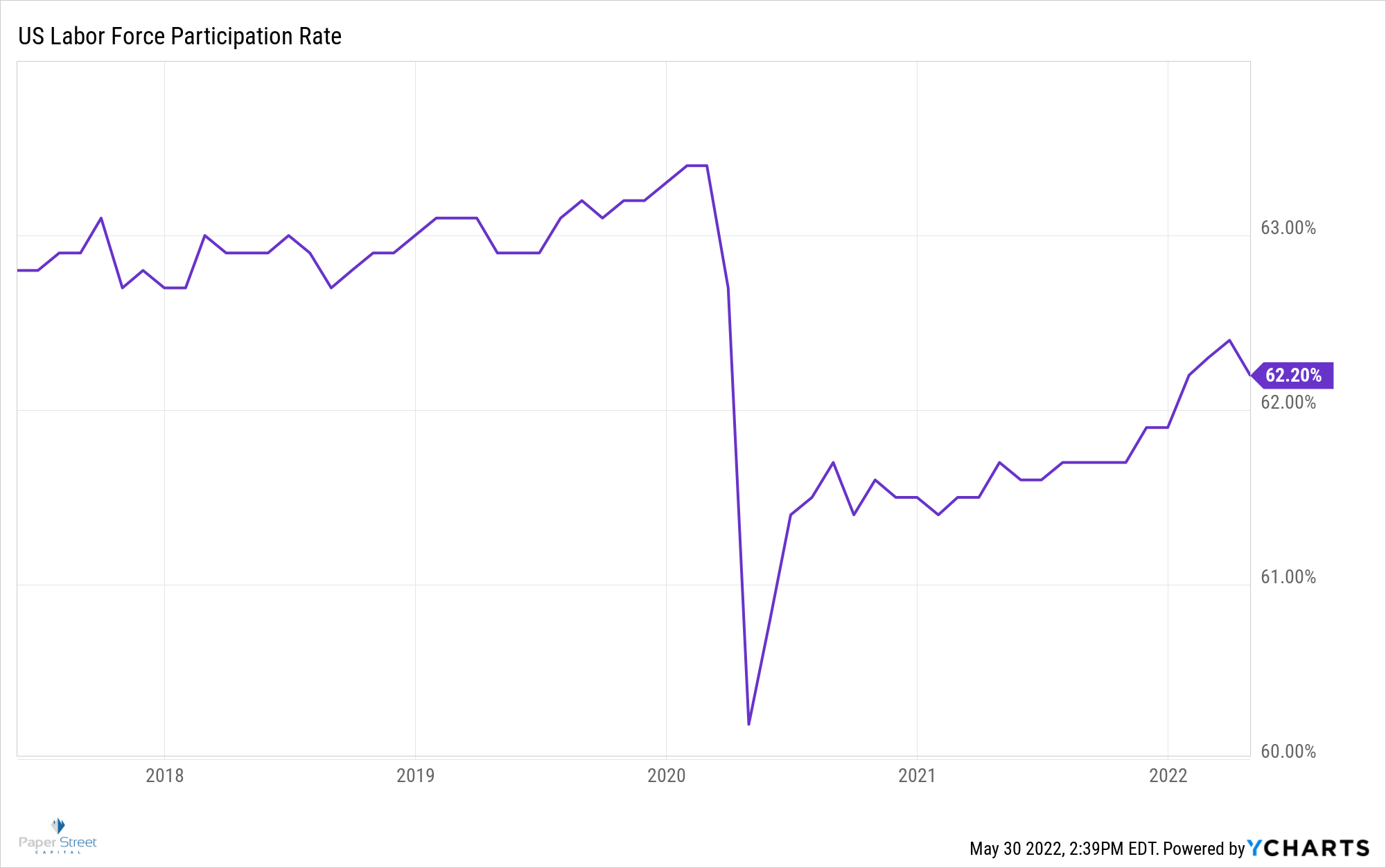

In normal times, a chart like this would seem good. Low unemployment and a job for everyone that wants one. Yet adding to this, the labor force participation rate is well off the 2019 levels:

Especially in areas like the south, where we’ve been “open” for at least 18 months now, I’m seeing little easing in the labor markets. There’s a missing piece to this that I can’t put my finger on, and I’m actively looking for an answer. In some ways, the answer may be a recession. For now, I’ve stuck with this puzzle for longer than I’m comfortable with, so here are some of the components that I think have been adding to the disappearance of everyone:

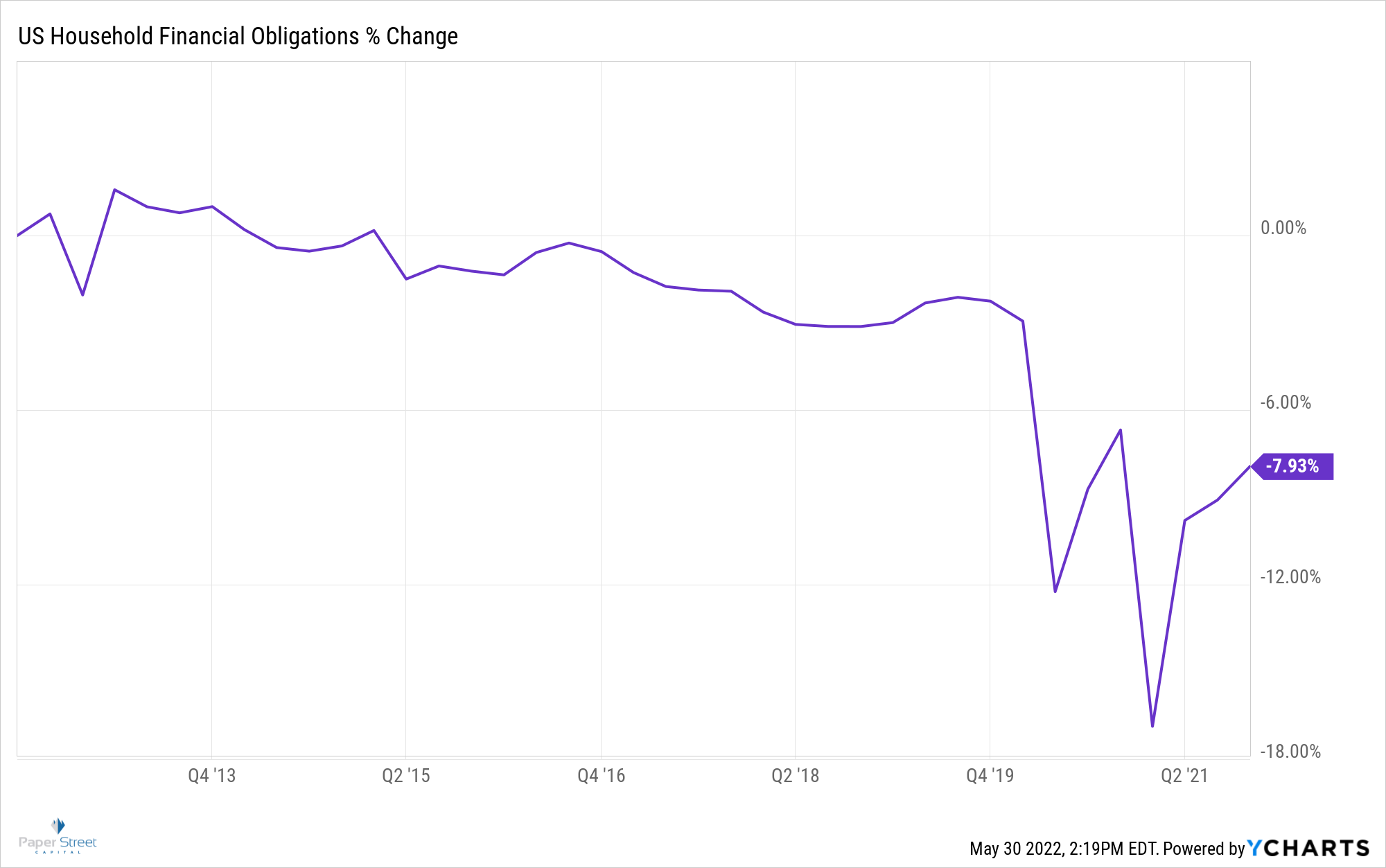

Lower Historically Relative Financial Obligations?

This was interesting to see, and it looks like this rate which is financial obligations as a percent of disposable income, has been slowly trending downward over the past decade:

This chart starts in 2011, and shows the slow and steady decline into early 2020 as the economic pre pandemic continued to improve relative to the past GFC years. Obviously financial obligations nosedived as stimulus checks went out, and most financial obligations like rent and mortgages were put on hold.

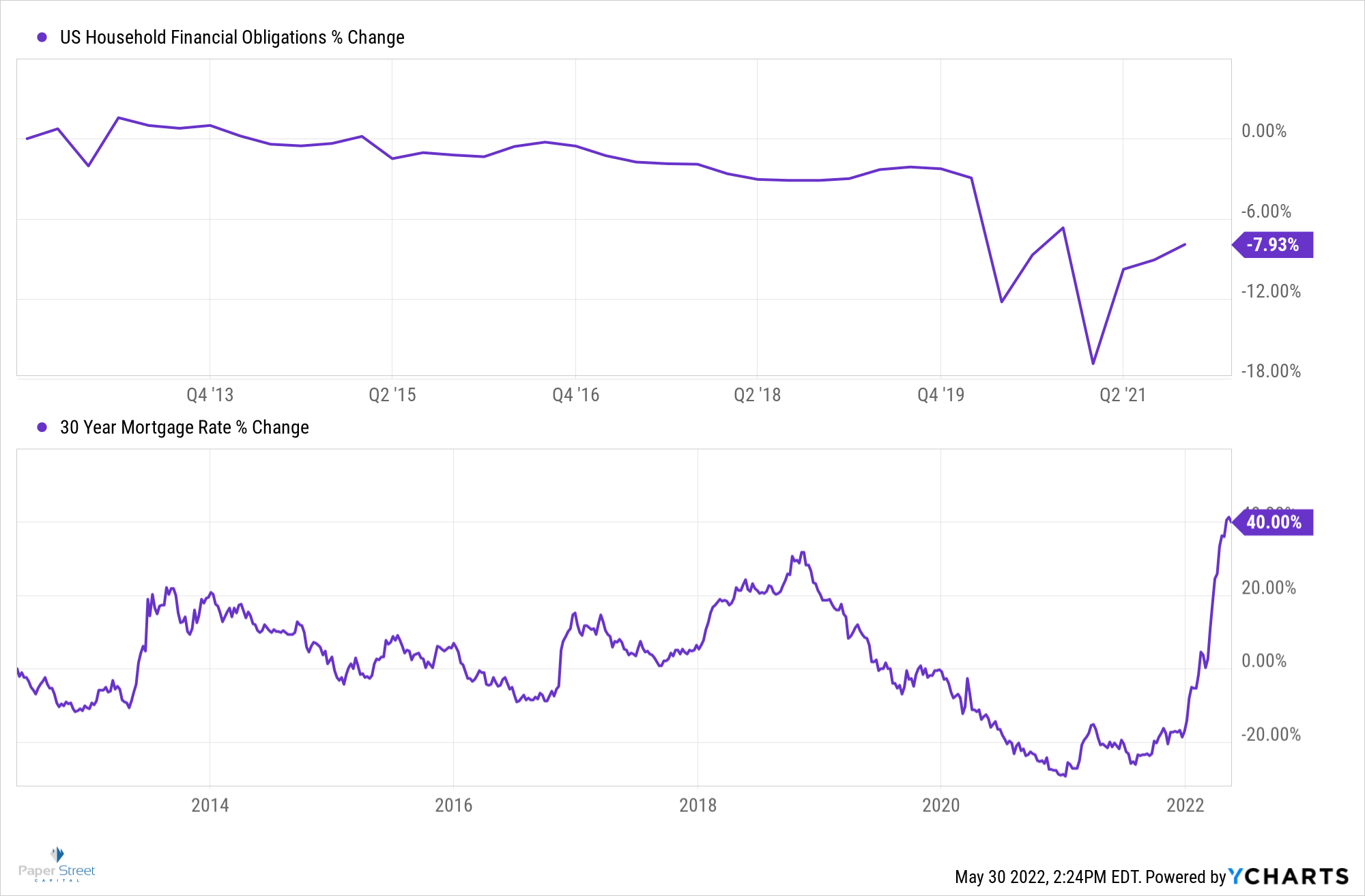

Into this year, this has increased closer to historical norms, but its well off the pre-pandemic levels. It is also important to note that the above data is only through Q4 of 2021. Sharply declining mortgage rates in the past few years may make up part of that decline, and suggest it may close to some degree soon as well:

So my thought process is there’s less urgency in the labor market because overall financial obligations are lower. This could be one of the components of the tight labor market.

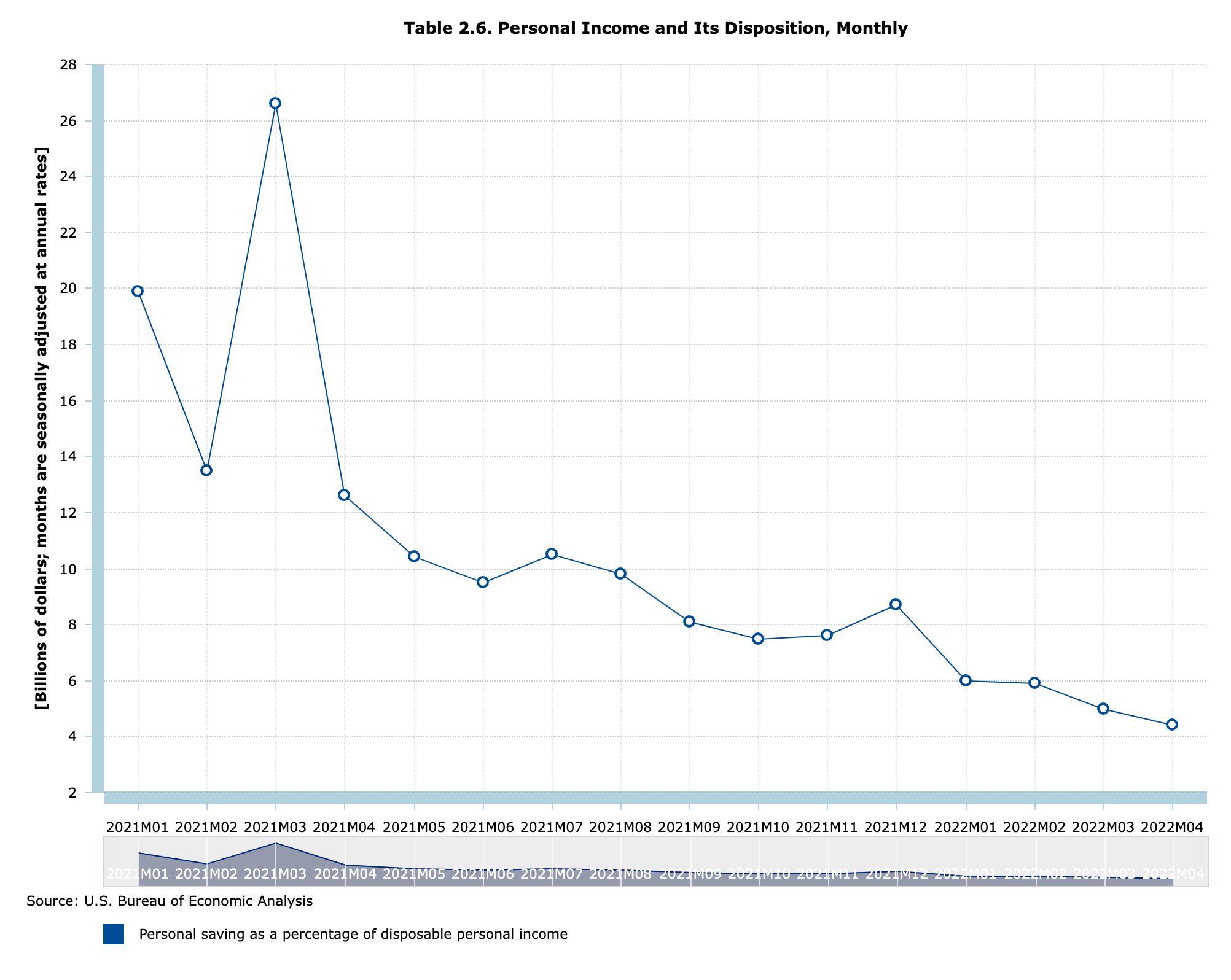

Then there’s signs that this window may be closing. Below is a chart of personal savings as a percent of disposable income, which is steadily declining:

The good news to the chart above is that maybe the counterbalancing urgency to get a job is making a comeback. This will be exacerbated as housing begins to cool (already starting) and the wealth effect from that asset plus 401k data pull people back into the labor pool.

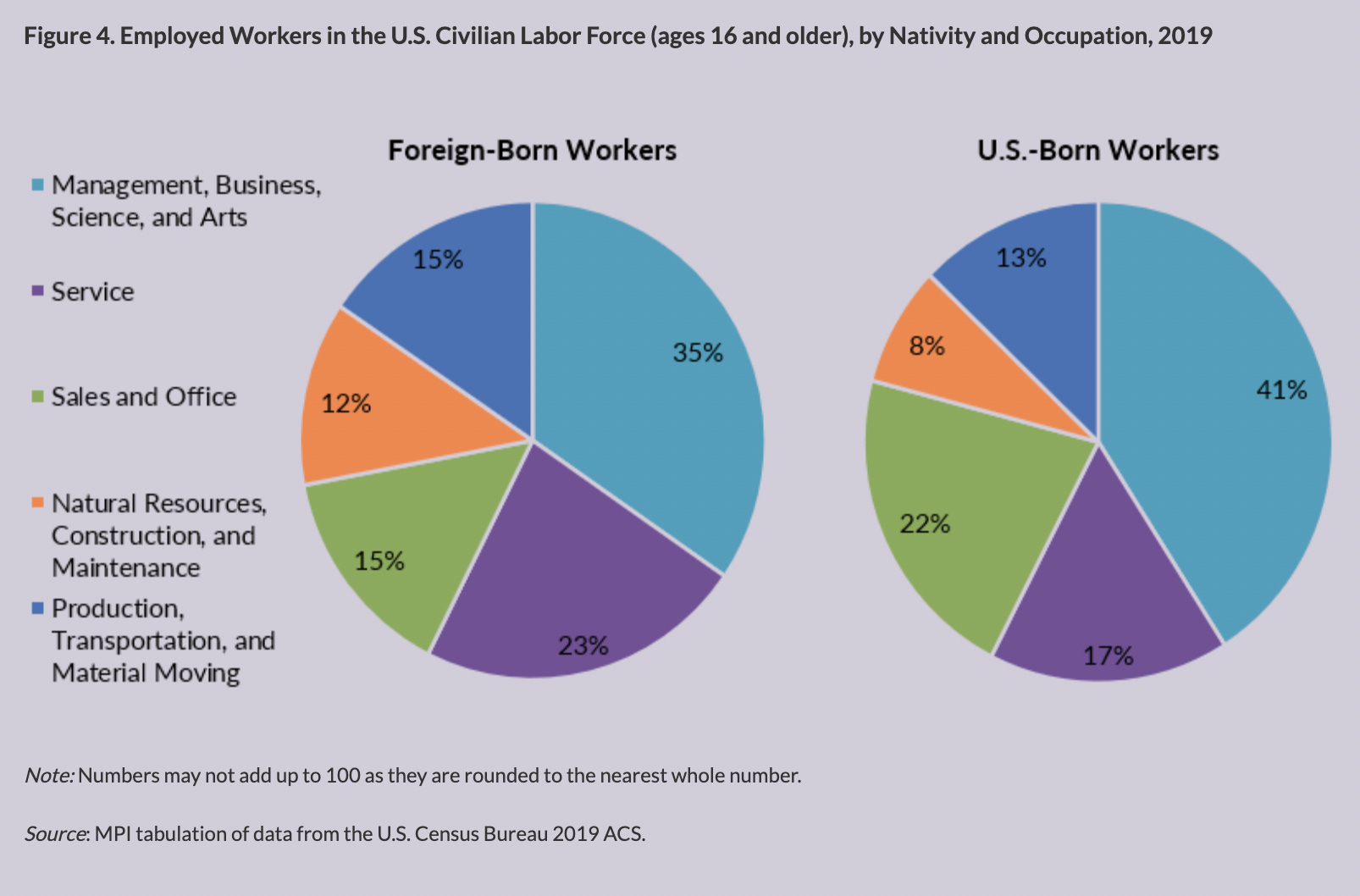

The net effect of limited immigration over the past coupe of years?

This could explain more than anything else, so stick with me. We effectively paused legal immigration since the pandemic. As the chart shows below, immigrants typically hold jobs in the more labor intensive sectors, which also generally incorporate the lower end of the income scale (services, construction, etc.):

With the pause in immigration around the world, what could have happened is positions usually held my immigrants were suddenly vacant. U.S. citizens who could move up the income scale, did or attempted to do so (elevated quit rates, costs of labor increasing). This left available positions for a native population who don't typically do those jobs, so they didn’t take them (explaining in part the elevated unemployment claims at times). It would seem though that as things opened, immigrant labor supply should have returned, and maybe they have, but its not showing up yet.

It still doesn’t explain the scarcity in more skilled labor. That will continue to be a mystery.

At the end of all of this, I think the conclusion I’ve come to is that regardless of the cause and effect of labor, I think the dislocations are coming undone, and we may be returning to a healthier labor market.

Labor had a strong upper hand for the better part of 18-24 months from elevated consumer demand, pent-up services demand from months of restrictions, and abundant liquidity that shored up financial obligations (which also added to the demand side). We are still experiencing elevated demand, but it looks like the Fed is getting good traction in removing excess liquidity out of the system. Several retailers like Walmart and Amazon (among others) have stated they are over staffed. So there’s a chance by the time I find my answers, it wont matter anyway.

I set out to answer the question I’ve have had on my mind for most of the pandemic, but at the end of it, I feel like I’m on a set of Penrose stairs. It seems like there’s fewer people working everywhere, but I can’t find out why. Where did everyone go? Or are they about to make a comeback?

We’ll have to see.

Will

https://www.wsj.com/articles/summer-worker-shortage-means-pools-camps-closed-11653918501?st=3t4x46072ist0d1&reflink=desktopwebshare_permalink