Primed For Success: Bancor in 2024

The road from disastrous to suddenly obvious

Note: I’m about to talk my book as an investor in BNT. As such, none of the following is investment advice or should be relied on as such. Moreover, all the following is derived from public information and may be imprecise in its interpretation. Accordingly, the following involves some degree of conjecture, and all opinions are my own.

The Current Deficit

To address the gorilla in the room, here’s a quick recap of the deficit:

This is a unique form of debt that the protocol incurred in 2022, which unlike normal forms of debt, is a non-cash expense that cannot be called, so it doesn’t pose an immediate threat to the business. It’s a relic of a previous business model that mirrored a form of insurance in which BNT was minted to compensate customer losses, known as impermanent loss protection. Unlike traditional forms of debt, the deficit is resolved merely by BNT outperforming specific assets.

It is important to reiterate that the deficit’s emergence resulted from fraudulent actors (such as the heads of Celsius, now in US prison, and Three Arrows Capital, currently in a Singaporean jail). They were at one time the largest participants in the protocol, prior to their individual destructions.

The downside is the “debt” is still on the books, however the upside is two-fold:

First, from an investor’s standpoint, the protocol is focused on creating and retaining value that accrues to the token such that the debt is resolved.

Second, and more importantly, when the deficit is resolved, massive token burns (around 25% of the outstanding token count) occur that further align the token structure.

Realigning The Token Structure

I spent the better part of the past 18 months reading various forms of financial history, from great books such as “Against the Gods: A Story of Risk”, “Panic: The Story of Modern Financial Insanity”, “How The Internet Happened” to more recently “The Company: A Short History of a Revolutionary Idea”.

What did I learn, specifically when it comes to the crypto space?

There is very little that is new.

What may feel novel is generally on the margins, especially when it comes to maintaining and generating value. There are base economic principles that cannot be violated, i.e. value must be contained, cultivated and used in a manner very akin to the laws of thermodynamics.

Just because tokens have the ability to be programmed, distributed, divided and held in somewhat novel ways, does not preclude them from obeying these economic laws.

This means, in part, limiting the “energy release” of mechanisms that result in unproductive value escape. This is best illustrated by dilutive mechanisms like airdrops, which for the uninitiated, are basically forms of mass dilution to a disinterested cohort who are looking to immediately sell your tokens.

It would be like Coca-Cola sending out shares to anyone who has the time to claim them, who then proceed to immediately sell them. This has become a cottage industry on its own; market participants who seek these opportunities to cash in on any protocol willing to play the game.

From an investor’s standpoint, it's as bad as it sounds.

Moreover, dilution in general is a scourge in the space, as many poor lessons were learned in the 2020-2021 era. Such lessons included “customers” seeking to be paid to use a service, and “investors” seeking risk-free money.

Both are calls to carefully choose your customers and investors alike.

I’m convinced a large part of the crypto markets are primarily a reflection of overall liquidity, as generally dictated by the Fed. Therefore, it’s important on two fronts to properly consider this dynamic:

First, don’t conflate an increase in prices as a direct reflection of the market’s acceptance of various developments or products. This is how poor lessons are ingrained and repeated.

Second, I sense it’s crucial to have your token structure correct, as when the tide inevitably comes rushing in, a protocol can benefit in an outsized manner just because of the increase in liquidity. Maybe it’s too simplistic, but I think it’s directionally correct, so simpler in this case is better.

So, what does a deficit resolution and sound token structure look like in terms of Bancor?

In short, it creates the architecture for a sound business model to thrive:

First, a deficit resolution, already well underway, has placed the token structure on a steady trajectory to a healthier state1:

In previous years, the BNT token supply was elastic in conjunction with its past business model that resembled an insurance product. When that all went sideways in mid-2022, token dilution was a real issue. Yet since that point, the outstanding token count has dropped by roughly 43%, a truly meaningful amount.

Second, a full deficit resolution has another roughly 34,600,000 in BNT set to burn, resulting in a roughly 25% decrease in token supply from today’s levels. This can happen very suddenly, as evidenced by the market activity in August and November which resulted in the immediate discharge of millions from the deficit:

Third, the protocol just embarked on using its roughly $4,000,000 Protocol Owned Liquidity (POL) to slowly repurchase and burn BNT. As part of the deficit resolution, this amount was in essence a form of retained earnings, which the DAO (Decentralized Autonomous Organization, a form of governance similar to weighted direct democracy) voted to use to further right-size the token structure. The first round of purchases occurred recently and is structured in the classical reverse Dutch-auction style, set to finalize over the course of the next three to six months.

Adding to that, the current business uses virtually all generated revenues to buyback and burn BNT. What this all signals is an alignment of current value production towards structuring the protocol into a vehicle that can best retain all future value created.

To quickly define value in this sense:

Customers of the protocol receive excess benefit from the offered innovation above the protocol fees. In short, a situation in which everyone benefits.

However, a sound token structure only matters in conjunction with a sound business model. The next key question then is, what is Bancor’s business model?

The Business Model

What has evolved over the past 18 months includes a business model that is focused on the few things that genuinely matter: sustainability, profitability, positive customer experience and innovation.

In my view as an outside investor, the protocol is moving towards a capital light, high margin business that focuses on leveraging and licensing its existing intellectual property (IP) and further developing new IP.

In a sense, it’s become a brain trust.

This business model monetizes its current intellectual property, while outsourcing larger distribution expenses via licensing deals. Again, back to my definition of value above, the parties that are licensing the product are happy to do so because it generates satisfied customers to their protocols.

As for the details of the licensing revenues, like most all similar such deals, they are non-public information. Yet crucially this route outsources distribution development costs to expand the product to other chains outside of Ethereum, while both Bancor and the licensee benefit. Moreover, it frees engineering and development efforts towards building new and innovative products (ex. research & development).

Directionally, Bancor is bucking the clown-car trends in crypto and adhering to historical economic principles.

No more paying customers to use a product, no more “free” money to token holders.

For the sane people who read that sentence and think that is blatantly obvious, this is not a common practice in crypto.

Business models matter, as well as how that organizational effort is returned back into the business. As stated earlier, choosing your investors and customers are key components to aligning everyone involved.

So is understanding who is at the helm.

My initial bet on Bancor back in September 2022 went something like this:

All of my best investments have been a bet on the team, a very subjective metric but one that hasn’t let me down yet. Where it was a bet on David Simon at Simon Properties when “no one would ever shop at the malls again” to Jane Elfers at Children’s Place when “children’s clothing was a dead business during the pandemic” or George Sherman, former CEO of GameStop when he took the helm of a company that seemed out of control but steadied the ship, and in that simple sense, that was all he needed to do, you know the rest of that story.

I can’t express it other than I get the same sense from listening and watching Mark Richardson over the past several months that we have at the helm a person I believe is on the pantheon of the greats when it’s all said and done. What makes me say that? I wrote about this when it was happening, but I don’t think most understand how difficult going on a call at the moment of a difficult decision to personally deliver bad news is. I personally haven’t done it to be fair, and as I wrote at the time, I’m not convinced yet that I have that courage. It was that leadership that I am sure would have taken out most everyone, yet to Mark’s credit he took 2.5 hours of questions and punishment.

And to be fair to the other Bancor members, like Nate, Jen, Yudi etc., they also all stuck it out with Mark and are all still here. And more to that point, if you’ve seen any degree of the swarm of negativity directed at these people, it would make anyone blush. It got so bad that even I, who had none of it directed towards me personally, had to make a few steps to not be exposed to it. Which brings me back to my initial point:

I love things that people love to hate.

Bancor quietly has one of the strongest bullpens of engineers, scientists, and entrepreneurs, all of which are all still there, now armed with hard-earned experience, heightened focus on risks, and true alignment of business principles in a world of circus mechanics.

That said, in accordance with primarily developing and licensing IP, as well as collecting a portion of revenue from use of its products (arbitrage or otherwise, as described later on), I sense the next logical step is to structure the cashflow in a manner that ensures sustainability of the business.

What I would like to see, as the token structure approaches its appropriate form and deficit eliminated, is for protocol revenue to shift from token repurchases towards business expenses such as payroll, legal expenses (ex. IP protection) and development costs. This very likely will be separate from the DAO, but as the debt resolution and token reshoring is adequately completed, I believe that revenue allocation must realign from the top down.

To the consternation of many crypto tourists, token revenue sharing must be at the bottom of the protocol stack, if it comes at all.

Question then is, where is the revenue coming from?

Innovative Product Suite

As Bancor appears to be moving towards the licensing business model by monetizing its IP, the fruits of that labor are as follows:

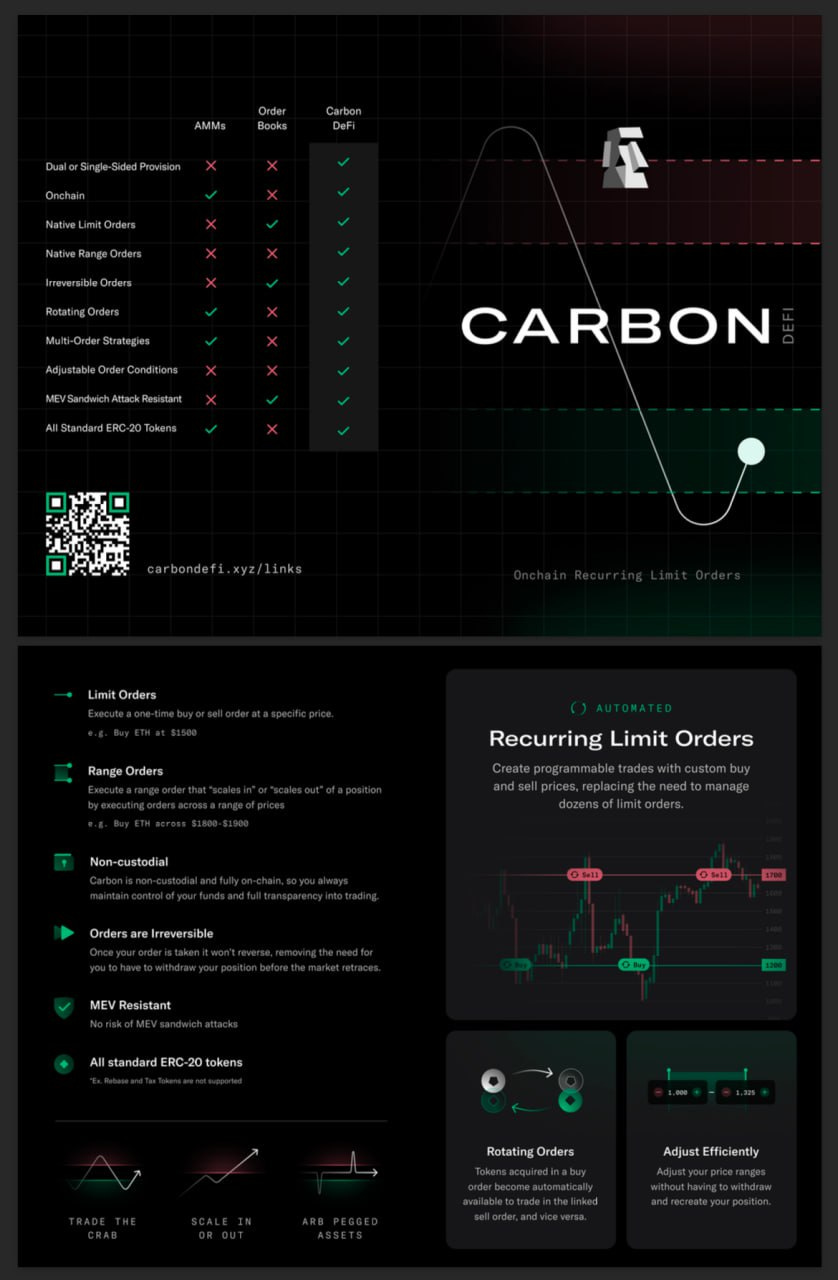

First, let’s start with the flagship product of Carbon2:

This patent-pending product solved a real problem in the on-chain trading world, true limit and range orders. It’s strange to say, but prior to Carbon if a market participant were to set an on-chain limit order… it could be reversed. That is a huge pain point in the industry that is now solved.

For purposes of this discussion, revenue generated on the product side is generally from a 20-basis point surcharge that is paid by the taker. However, the primary customers of Carbon are makers in the exchange, as best illustrated below by the maker who sets the asking price3:

In conjunction with Carbon, another product of innovation from Bancor this past year is one I’m genuinely excited about:

The Arb Fast Lane4:

Fast Lane is a protocol that allows any user to perform arbitrage between Bancor ecosystem protocols and external on-chain exchanges and redirect arbitrage profits back to the Bancor ecosystem. With Fast Lane, Bancor ecosystem protocols can now internalize arbitrage profits that in other DEXs are lost to external agents like arbitrage bots and MEV bots.

In essence, the Arb Bot participates in what I have gathered to be a part of the market that, while highly competitive, is also highly profitable… arbitrage.

This is very true in the traditional finance sector, and no different in the Web3 space.

Moreover, the Arb Bot’s mechanics augment Carbon, further complimenting Bancor’s overall business model. Use of the Fast Lane Arb Bot helps recapture value that was otherwise lost in the decentralized finance space.

Again, a focus on creating, capturing and retaining value back into the business.

While licensing Carbon and the Fast Lane protocol bring in undisclosed benefits to Bancor, it’s important to note that the Fast Lane Bot returns 50% of the profits directly into the protocol. For instance, here is a sample arb from just the other day:

The “caller” in this example is a benefit of the open-source nature of this product. This is the person/entity that is running the protocol with their own hardware and benefitting from the development expenses incurred by the Bancor engineering team. Again, its profit split mechanism encourages many people, both professional and novice, to run the arb bot at their leisure.

The caller receives $122.17 (and pays the gas expenses).

The protocol receives $122.17.

Everyone wins. Over and over.

This design choice, like the licensing route, helps outsource more costs and widen overall reach.

Primed for Sudden Success

In sum, Bancor’s alignment with historical principles of sound business models, operating within a token structure that both captures and preserves its created value, driven by a bullpen of engineers and scientists with a history of innovation, I believe is a recipe for long term success.

In my mind, the token structure is well on its way to be right sized by means of all current revenue used to buy and burn excess tokens and a full deficit resolution. Removing this excess slack helps remove disinterested “investors”, tourists and non-aligned participants.

My investment in Bancor has always been a bet on the high-quality people behind the project. In simple terms, the creatives have an excellent track record of innovation, have gone through serious turbulence, and are coming out much more dynamic than they ever would be otherwise.

I sense we’re currently in a phase that is part restructuring, part growth. What it also means is that once the deficit is resolved, the protocol will be better set to leverage, maintain and generate value for all involved.

Further, I believe it has the potential to be suddenly successful:

The sudden success comes from a deficit resolution that suddenly realigns the token structure by shrinking it by a factor of 25% or more.

The sudden success of an arbitrage bot that produces more profits than the protocol ever experienced since its inception.

The sudden success of Carbon being used by the largest market makers in the space by way of licensing the contracts.

The sudden success of a business model based on licensing intellectual property that is capital light and high margin.

Altogether, I believe it will shift the public view of Bancor from previously disastrous to suddenly obvious.

And who doesn’t love a comeback story?

Will

https://dune.com/bancor/bancor-v2

https://resources.carbondefi.xyz/pages/CarbonLitepaper.pdf

https://dr-fee.com/blog/maker-vs-taker-fee

https://bancor.network/arb-fast-lane